Floods are the most common and costly natural disaster in the US. According to the NFIP, 90% of natural disasters in the US involve flooding. And, flood damage restoration is expensive to repair. FEMA states that 1 inch of water can cause $27,000 in damages to a 2,000 square foot property. With the potential and high cost of flooding incidents, purchasing flood insurance for your home or business is crucial.

Flood insurance is excluded from most property insurance policies. It is a separate policy purchased through the National Flood Insurance Program (NFIP) and is required in many areas. Flood insurance is required for properties located in areas at high risk of flooding when obtaining a mortgage from any federally backed lender. Just because you don’t live in a high-risk area or haven’t experienced a flood doesn’t mean you never will. According to FEMA, “a quarter of all flood insurance claims are submitted by policyholders in low-to-moderate risk areas, and policyholders in high-risk zones have a 26% chance of experiencing a flood over the life of a 30-year mortgage.” Still, many people overlook its importance.

Let’s take a look back at Hurricane Harvey from August 2017. The storm caused over $125 billion in damages, making it the second costliest hurricane to affect the US in history. Harvey dropped as much as 60 inches of rain and brought in over 11 ft of storm surge in some areas. FEMA states that 80% of households affected by Harvey weren’t covered for floods. In Harris County, Texas alone, only 36% of those who flooded had flood insurance because most of the homes were outside the 100-year floodplain.

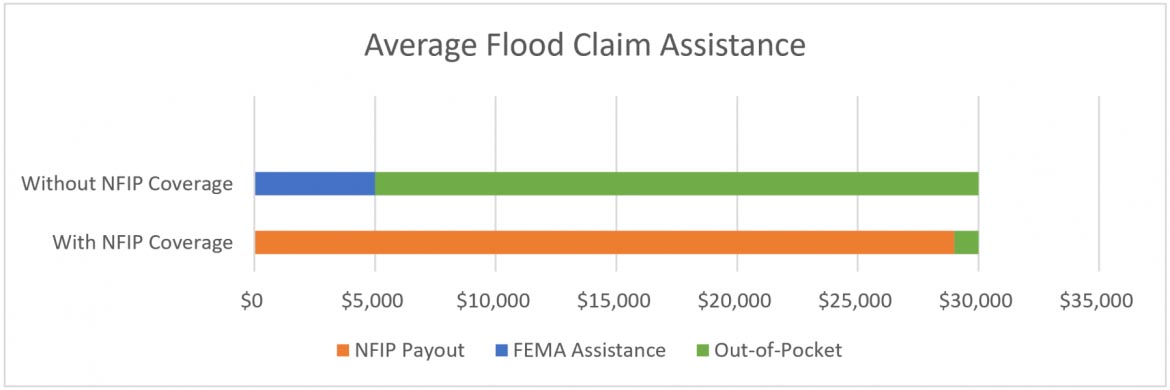

Although property owners without flood insurance who have been affected by flooding can apply for federal assistance through FEMA and the SBA, the amounts provided frequently aren’t enough to cover the cost of repairs. In addition, these federal disaster assistance programs are only available if the president declares a federal disaster. FEMA provides around $4,000 to $7,000 on average per household, which is far less than the average cost of a homeowner flood claim at $30,000 or commercial flood claim at $85,000. Homeowners who flooded during Hurricane Harvey but had flood insurance received, on average, more than $100,000 more to rebuild than their neighbors who relied solely on FEMA benefits.

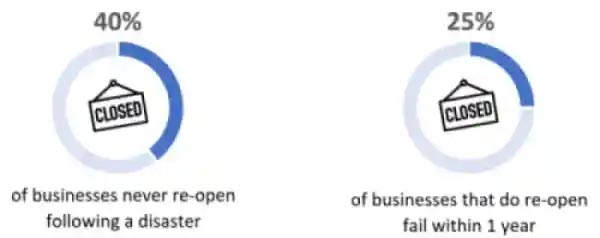

The SBA offers disaster assistance to businesses through loans that must be paid back with interest, which can put strain on a business already struggling to pay for repairs. 40% of businesses do not reopen after a disaster, and another 25% that do reopen fail within a year.

t is important to remember that flood policies go into effect 30 days after purchase. Also, the NFIP limits coverages to $250,000 for buildings and $100,000 in contents coverage for homeowners, and $500,000 building coverage and $500,000 in contents coverages for businesses. Contents are covered for actual cash value under NFIP policies, which is the value of the item at the time it’s lost, not the original purchase price. If you own a high-value building, you can often purchase third-party supplemental insurance to cover the difference.

For properties not located in high-risk flood zones, flood insurance is very reasonably priced. The average cost is around $395 per year for the NFIP’s Preferred Risk Policies. This means, you would need to pay for the insurance policy for 76 years before you would reach the out-of-pocket expense equal to the average homeowner flood claim.

If you live or work anywhere near areas prone to flooding, please consider purchasing flood insurance. Doing so could save you from tremendous out-of-pocket expenses to repair your home or business. Talk to your local insurance agent to find out if flood insurance is available in your community, and what the annual cost will be before disaster strikes.